Inflation changes how businesses survive. It raises the cost of materials, disrupts supply chains, and lowers customer spending power. However, inflation does not impact all retail businesses in the same way.

The impact of rising costs depends entirely on business structure, customer relationships, and supply chains. Direct-to-Consumer (D2C) brands and traditional local neighborhood retailers, known as kirana stores in India, face completely different challenges during inflation.

While a kirana store fights localized price resistance, a D2C brand faces systemic threats to its unit economics, digital acquisition model, and venture-backed survival.

1. Supply Chain Structures and Cost Absorptions

The fundamental difference between D2C brands and kirana stores lies in their supply chain structures. This variance dictates how each entity experiences rising producer prices.

D2C Brands: The Weight of Upstream Volatility

D2C brands control their entire value chain, from raw material sourcing and manufacturing to final packaging and delivery. When inflation strikes, a D2C brand experiences a compounding cost effect across multiple stages:

- Raw Materials: Rising commodity prices instantly elevate production costs.

- Specialized Packaging: Custom, branded packaging incurs higher paper, plastic, and printing costs.

- Logistics and Warehousing: Fuel inflation directly increases third-party logistics (3PL) fees and fulfillment center storage rates.

Because D2C brands operate without intermediary wholesalers to absorb these shocks, the entire inflationary pressure hits their gross margins immediately.

Kirana Stores: Shielded by Fast-Moving Consumer Goods (FMCG) Giants

A kirana store operates as the final link in a highly optimized mass-distribution network. They source finished goods directly from local distributors or cash-and-carry wholesalers.

- Leveraging Conglomerates: Major FMCG conglomerates absorb the initial shocks of commodity price spikes through scaled hedging and global procurement.

- Grammage Reduction: Instead of raising the price of a standard retail unit, manufacturers frequently deploy “shrinkflation” reducing the product volume while maintaining the visual packaging and price point (e.g., shrinking a ₹10 biscuit packet from 100 grams to 85 grams).

- Price Protection: The kirana store continues to sell the item at the exact same price point, completely insulated from consumer backlash regarding price increases.

2. Customer Acquisition and Retention Economics

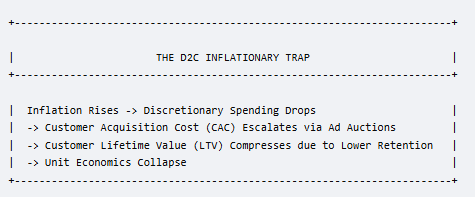

Inflation alters consumer psychology, shifting spending from discretionary items to absolute necessities. This shift disrupts the customer acquisition metrics that govern digital commerce.

D2C Brands: The Customer Acquisition Cost (CAC) Trap

D2C brands rely heavily on targeted digital advertising (e.g., Meta, Google) to acquire customers. During inflationary periods, this model suffers from a double-sided squeeze:

- Diminishing Ad Efficiency: As consumers tighten their wallets, ad click-through and conversion rates drop significantly.

- Escalating Auction Costs: Ad platforms remain highly competitive, causing CPMs (cost per thousand impressions) to rise or stay flat while conversion performance drops.

- Compressed Lifetime Value (LTV): Inflation drives consumers to switch down to cheaper alternatives, destroying the repeat-purchase rates that D2C brands need to recover their initial CAC.

Kirana Stores: Zero-CAC Organic Footfall

A kirana store does not pay to acquire customers. Its customer acquisition cost is zero, structurally built into its physical location within a residential community.

- Geographic Monopoly: Consumers walk to the local store out of sheer convenience and immediate necessity.

- High Retention: The store does not need to run digital remarketing campaigns to bring a customer back; local proximity ensures repeat footfall.

- Inelastic Demand: The inventory consists primarily of daily essentials (milk, bread, pulses, soap), which consumers cannot cut from their budgets, even during high inflation.

3. Pricing Agility versus Sticky Consumer Perceptions

Adjusting prices to protect margins is a delicate balancing act during inflation. The two retail models possess vastly different levels of pricing flexibility.

D2C Brands: High Visibility and Rigid Expectations

D2C brands sell premium, differentiated, or lifestyle products. Altering prices online creates immediate friction:

- Transparent Pricing History: Digital consumers can easily track price changes, compare across e-commerce marketplaces, or wait for coupon codes.

- The “Premium” Premium: Because D2C goods are already priced higher than mass-market alternatives, any additional price hike risks pushing the product past the consumer’s threshold of discretionary value.

- Tech Overhead: Changing prices requires updating digital storefronts, active ad creatives, and affiliate networks, which can lead to friction in multi-channel operations.

Kirana Stores: Fluidity Through Relationship Banking

Kirana stores sell unbranded or loosely packaged commodities alongside branded FMCG goods. This allows them unique hyper-local pricing agility:

- Micro-Adjustments: A kirana owner can raise the price of loose flour, rice, or loose spices by small fractions based on morning wholesale market rates without changing any visible price tags.

- Informal Credit (The Khata System): To counter consumer price resistance, kirana stores deploy informal credit. By allowing trusted customers to buy now and pay at the end of the month, the store retains volume sales and defers the consumer’s immediate cash-flow pain. D2C brands cannot offer informal, interest-free credit lines to anonymous internet shoppers.

4. Working Capital and Inventory Management

Inflation erodes purchasing power, making cash flow management the ultimate test of business survival.

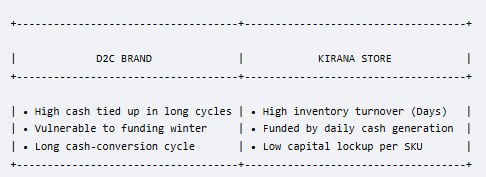

D2C Brands: Capital Lockup and Long Cycles

D2C brands must manufacture in bulk batches to achieve economies of scale.

- Extended Lead Times: Cash is locked up in raw materials, manufacturing, and transit weeks or months before a sale occurs.

- The Valuation Squeeze: Many D2C brands operate on venture capital or debt. Inflation triggers higher central bank interest rates, causing capital markets to dry up. A D2C brand with extended cash-conversion cycles can quickly face insolvency if its burn rate outpaces its squeezed margins.

Kirana Stores: Just-in-Time, High-Velocity Retail

A kirana store operates on an incredibly tight, efficient cash-conversion cycle.

- Daily Cash Velocity: Stock turns over rapidly. Fresh produce, dairy, and high-demand staples generate cash daily.

- Low Minimum Orders: Distributors deliver to kirana stores multiple times a week, allowing the store owner to buy inventory in tiny fractions.

- Dynamic Capital Allocation: If the wholesale price of a certain oil spikes, the store owner simply buys fewer units of that brand and shifts capital to a faster-moving or higher-margin staple. They carry minimal capital risk per stock-keeping unit (SKU).

Final Takeaway: Two Divergent Paths to Survival

Inflation exposes the fundamental structural differences between modern digital commerce and traditional retail.

For the D2C brand, inflation is an existential threat to its core business model. It strikes at their unit economics by inflating manufacturing costs while simultaneously driving up digital acquisition costs in an environment of shrinking discretionary spending. To survive, D2C brands must abandon hyper-growth metrics, rationalize their SKUs, optimize logistics, and transition into multi-channel physical retail where customer acquisition is more stable.

For the kirana store, inflation is an operational friction rather than a structural crisis. Protected by FMCG manufacturers’ shrinkflation tactics, zero acquisition costs, inelastic neighborhood demand, and the social collateral of informal credit, the kirana store remains highly resilient.

Ultimately, while inflation forces D2C brands to fundamentally reinvent their financial structures, it simply requires the local kirana store to do what it has always done best: adapt its margins, trust its community relationships, and manage its daily cash flow.